Transition to a Multipolar monetary order is happening faster than anyone could have expected. Yesterday it was announced that China trades more in RMB than in USD. This is a significant achievement as it means China needs fewer dollars and fewer dollar reserves for stability or interventions. This comes 3 weeks after it was reported that Russia FX trading in RMB exceeds USD on the Moscow Exchange. Two of the largest economies on the planet are now aligned in RMB as their preferred and dominant currency.

China is the largest trading partner for 140 nations. As these nations shift to trade in RMB rather than USD the second order implications become important for global credit, capital markets, and financial stability.

- Demand for USD credit and assets will diminish.

- The sanctions weapon the US Treasury has wielded against 40 nations will cease to have much impact.

- US Treasuries will lose global creditor flows as more nations will reserve less in dollar, needing dollars less.

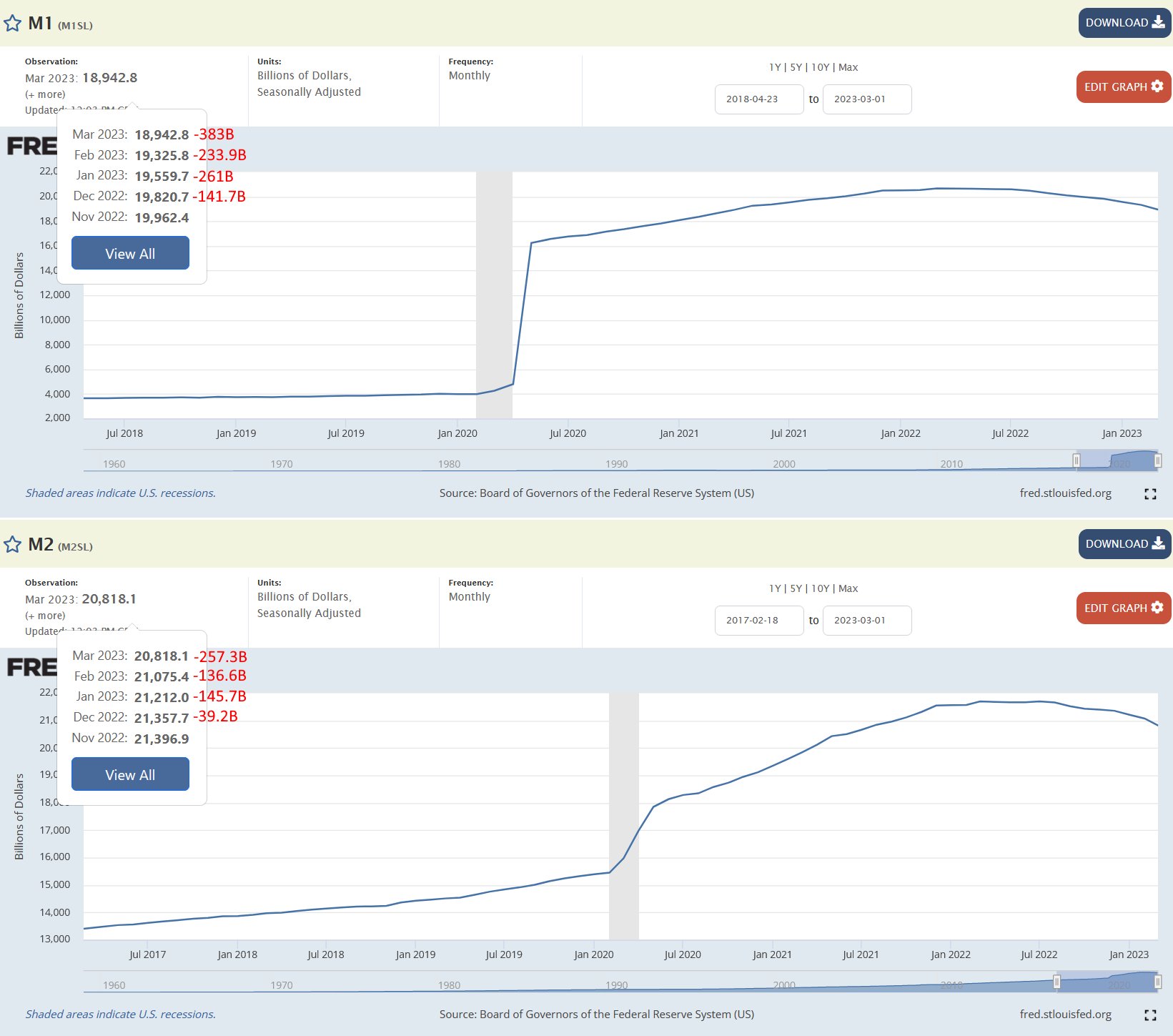

Already M1 and M2 have seen contraction at record rates. The reduced need for dollars and dollar claims may be part of this story if foreigners withdraw deposits and cash-substitutes from the US economy. It is likely not a coincidence that M1 peaked as sanctions on Russia were announced. Foreign ownership of US Treasuries peaked in 2021, and the case for accumulation of further holding is much worse today. Bonds have taken a valuation mark down.

Bank deposit outflows are stressing the US banking system. Some of these deposits in M1 have shifted to money market funds, an element of M2, but not all. Many appear to be leaving the US altogether. Outflows accelerated after the recent bank failures, doubling month-on-month from February to March.

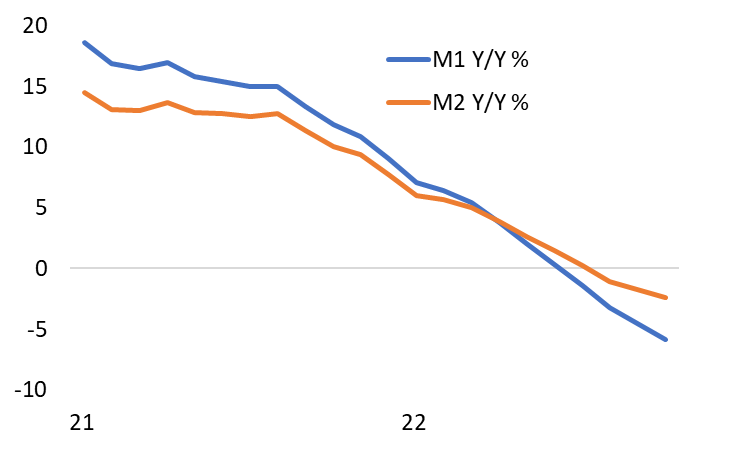

The chart below shows the same M1 and M2 data as year-on-year change in percentage terms.

Tighten your seat belts. The transition to a Multipolar monetary order could get bumpy from here.

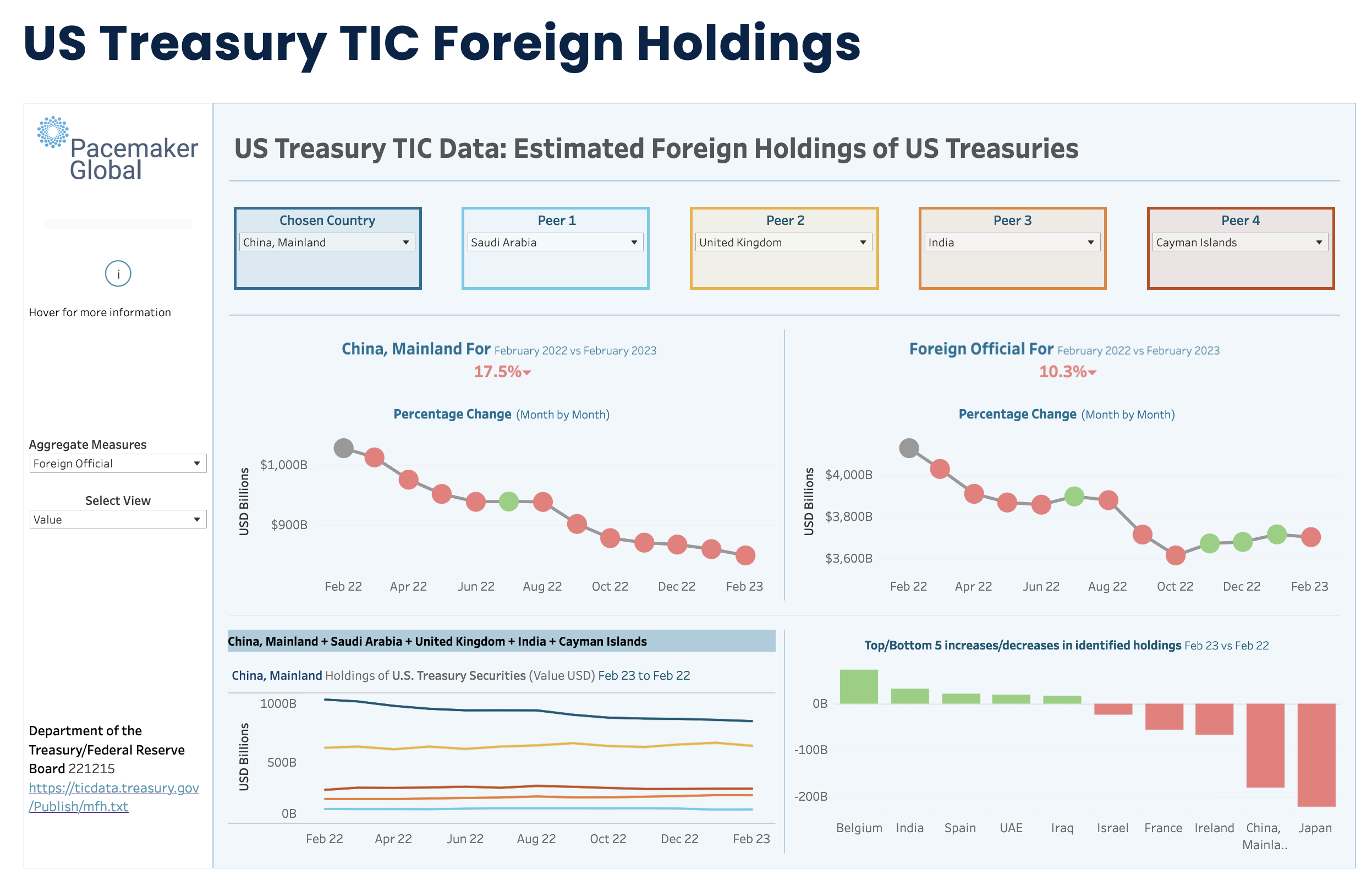

Two Pacemaker Tools on the Data page (SignUp required) are relevant to this shift. The TIC Tool monitors monthly shifts in Foreign Holdings of US Treasuries as a proxy for foreign demand for US liquidity. Foreign Official holdings (central bank reserves) were down $450 billion to end-2022. China's holdings of USTs have been declining with the share of trade in USD.

Our WTO Tool allows you to explore top trade partners in all import categories. This can be useful to prioritise trade evaluation in alternative currencies, and prioritise trade partners for negotiations.