The first story I read on Bloomberg this morning was Didi Loses $22 Billion in Market Cap After China Crackdown. Later in the day I read the Shuli Ren commentary, also on Bloomberg, The Tiger Who Came to Tea — Didi-China Style. These seem to me rather unfair to China, and rather one-sided about who was to blame for misleading investors in New York.

If you read other sources you learn that Didi's management was called into a regulatory briefing over 3 months ago where they were warned to clean up their act about data protection, cyber security, and other compliance issues. The Chinese cybersecurity authority also suggested some weeks ago, before it was announced in New York, that Didi delay its planned IPO.

Perhaps because of what happened with Ant Financial pulling its IPO last year, Didi's management, existing investors, and American investment bank underwriters accelerated the IPO instead.

This was all well known to everyone in China.

There is quite a lot missing from the Bloomberg coverage.

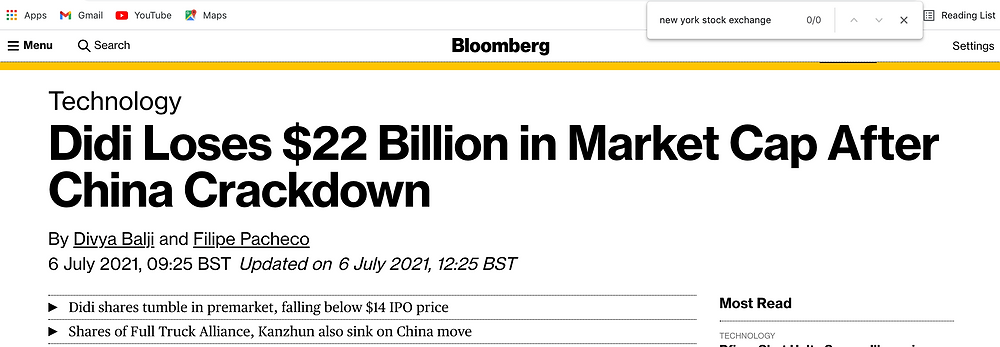

First, Bloomberg coverage omits the name of the exchange where Didi listed; it was the New York Stock Exchange. The exchange will be responsible for listing and prospectus rules, and ensuring advance compliance by new listings for IPOs. If Didi's management and underwriters withheld the information about the Chinese regulatory interest and investigation, and indeed the supervisor's suggestion that it delay the IPO, that would seem out with what I know about US prospectus, material disclosure, and exchange listing rules. The screenshot below shows 0 hits for 'new york stock exchange' in the principal Bloomberg story.

The Bloomberg article and commentary coyly refer to 'New York' and 'US markets' rather than name the NYSE, the exchange responsible for vetting the listing against its own rules. Then the Bloomberg piece discusses a NASDAQ index for Chinese listings.

Second, the Bloomberg article and commentary omit to name the underwriters, or even the lead underwriters, of the Didi listing. They were Goldman Sachs, Morgan Stanley, and JP Morgan. Didi management might be forgiven for unfamiliarity with US prospectus and listing rules, but the top investment banks of Wall Street have no such excuse.

Third, the Bloomberg coverage omits that Softbank was the foremost shareholder, owning more than 14 percent of Didi, and most keen to exit from Didi through the IPO.

So the Chinese regulators warned the company that it was under investigation for poor data security practices over 3 months ago. They asked the company's management to delay the US listing weeks ago. But Bloomberg wants us to believe that somehow it is the Chinese authorities who are at fault and taking aim at poor, vulnerable US investors by finally taking supervisory action on 2nd July to curb Didi acquiring new customers until it corrects supervisory failings.

I'll be reading Bloomberg's China coverage more sceptically in future.