I am a plumber of global liquidity. I watch flows and worry about systemic risks. I started working on Pacemaker in July 2019, seeing the US Treasury market vulnerable to enduring dysfunction. Rising inflation limits the scope for effective central bank intervention. US regulators stymie meaningful reform. This creates systemic risk globally as almost all fixed-income dealers and platforms quote spreads against USTs as the 'risk free rate'. New York Fed on 15 November 2022: Liquidity in USTs is as bad as March Madness 2020.

The first market failure came in September 2019. Overnight repo rates spiked to 10 percent for no obvious reason. The instability forced the Federal Reserve to reverse course on quantitative tightening, flooding money back to the market.

The US Treasury market failed almost entirely in March 2020 after the pandemic hit. Dealer screens went dark, no quotes. That communicated panic around the world as other fixed-income markets lost pricing, quotes, order books, and liquidity within seconds. A BIS report on the 'March Madness' made various recommendations and the Fed undertook a review.

Since then more than $9 trillion of Fed QE has funded US federal spending and market support. The US Treasuries market has hobbled along, increasingly illiquid, over-pressed with new issuance for pandemic stimulus, Ukraine-related spending, and midterm election pork. It's too much debt for market capacity, and the structural strains are beginning to show.

Let's look at what the New York Fed says:

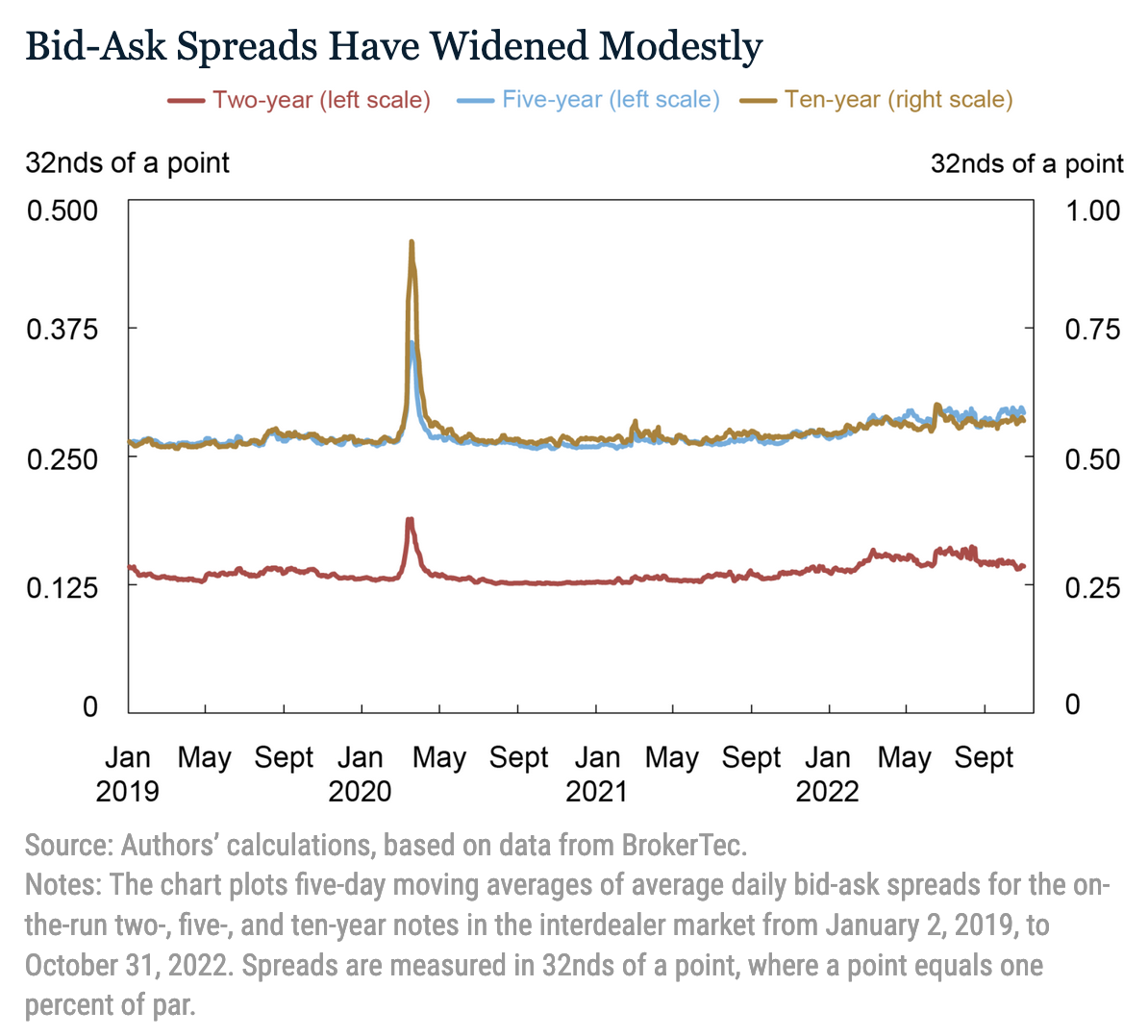

Bid-Ask Spreads Have Widened Modestly

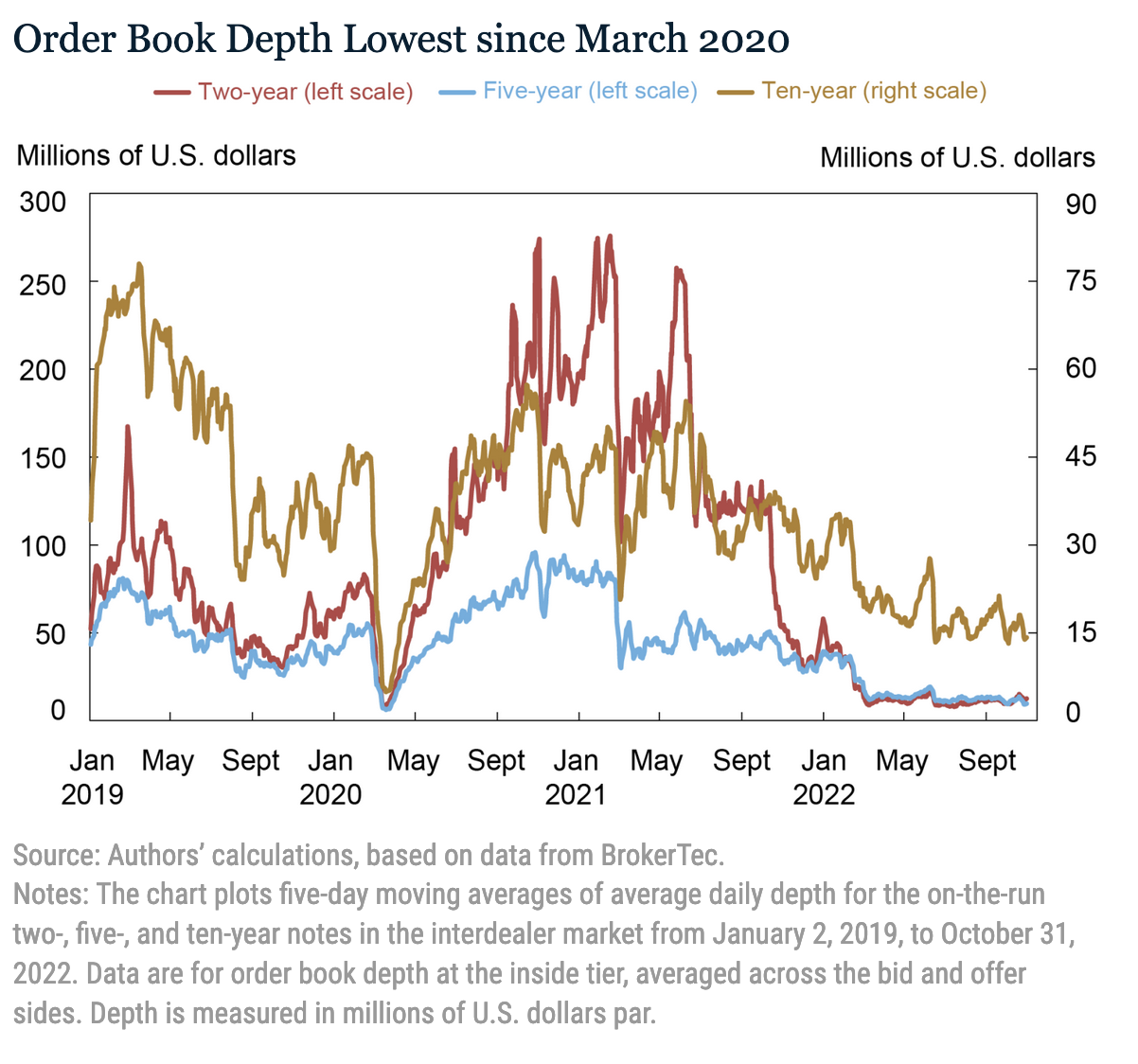

Order Book Depth Lowest since March 2020

Price Impact Highest since March 2020

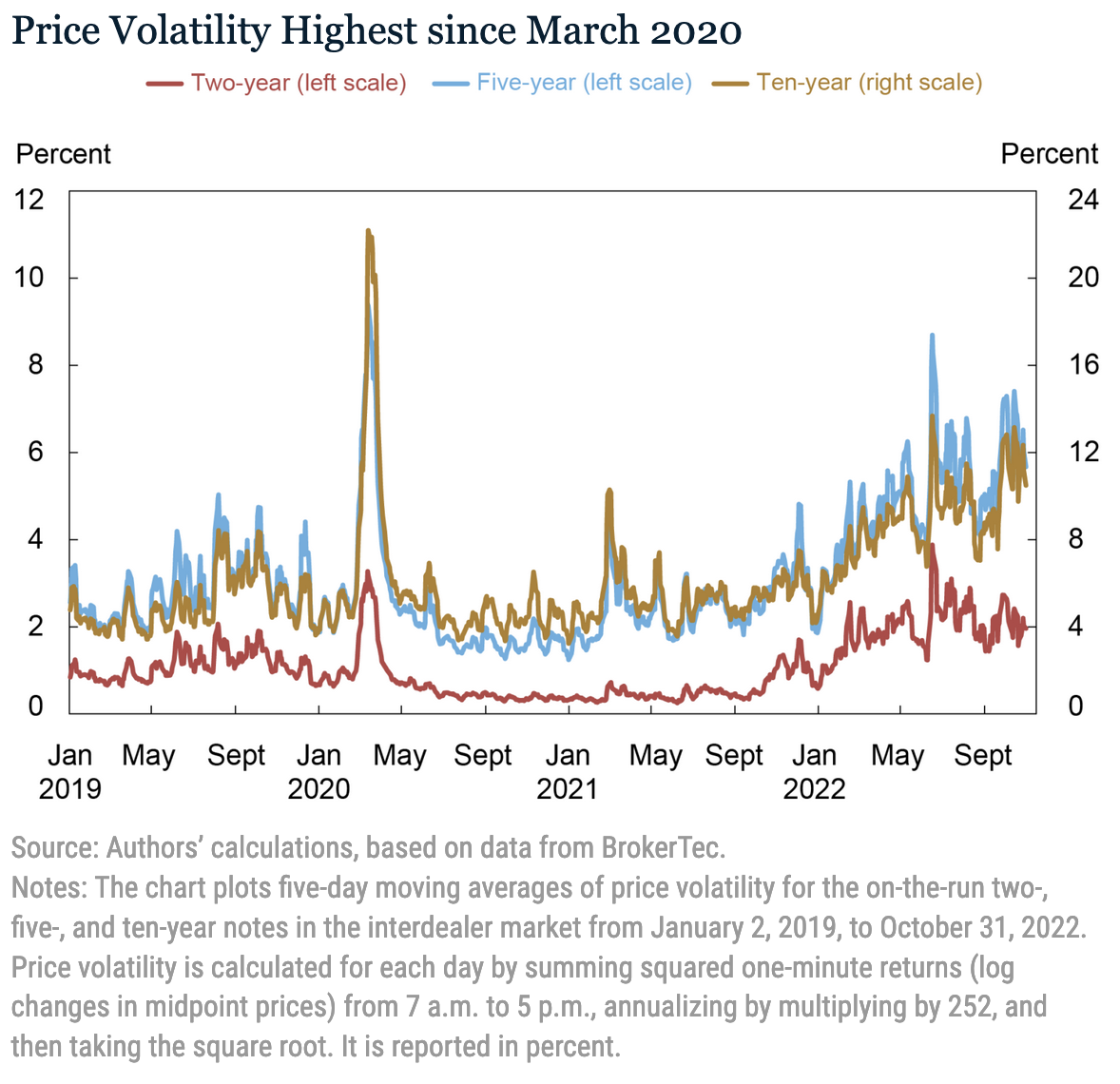

Volatility Has Also Been High

Trading Volumes are High consistent with Stressed Markets

The Treasury, Fed and SEC have adopted a series of policies over the past 20 years that cumulatively undermined dealers' commitment to the Treasuries market, dealer inventories, and ability to trade in size with minimal price impact and volatility. Because the same policy makers that made these calls were convened to review the market (they're the 'experts'), sensible reforms to reverse the damage are unlikely. Instead, the Inter-Agency Working Group have recommended doubling down on policies I think misguided and harmful, like mandatory CCP clearing (skews initial margin as punitive to medium and small dealers, forcing them from the market) and post-trade transparency (undermines dealing in size and promotes price volatility). I disagree with a lot more of their policies, but detailing each would make this a very long book instead of a blog.

I'll leave the conclusion to the New York Fed economists:

[L]ower-than-usual liquidity implies that a liquidity shock will have larger-than-usual effects on prices and perhaps be more likely to precipitate a negative feedback loop between security sales, volatility, and illiquidity.

In March 2022 the BIS Markets Committee published guidance on new tools for intervention in markets, favouring a 'backstop principle' of targeted, time limited intervention. This is what was used by the Bank of England in September when gilts crashed, and it worked pretty well. Whether the Fed could do the same for US Treasuries is open to question. And doesn't really solve the problem that the world's most liquid market is no longer reliably liquid, the basis for global pricing no longer reliably prices.

As global fixed-income markets are normally quoted as a spread on Treasuries, policy makers should consider the implications of continued illiquidity, price volatility, and dysfunction as a systemic risk that could communicate to their own markets. This is a global systemic risk.